Route Air Navigation Charge

Decree n° 2-73-035 of safar 10th 1394 (march 5th 1974) -conjoined Order of the Minister of public works and communications and of the Minister of finances n°276-74 of safar 14th 1394 ( march 9th 1974)

1.The use of the installations and services of en-route air navigation,

The use of the installations and services of en-route air navigation, including services of radio-communications and meteorological, that the State implements in airspace under its responsibility, as it is defined by the International Civil Aviation Organisation, for the safety of en-route air navigation and the speed of its movements, entails a remuneration in the form of a charge for rendered services, called « route charge ». The charge constitutes a remuneration for the costs supported by ONDA within the flight information region of Casablanca, taking into account the use of the installations and services of en-route air navigation. The due charge is paid by the aircraft operator, or if he is not known, by the owner of the aircraft. The charge shall be collected from all flight effected within Moroccan airspace, to the exception of exonerated flights. The determination of the charge amount is determined based on covered distance within the airspace, maximum take-off weight and unit rate.

2. Calculation formula

The amount of en-route charge (R1) for a given flight is equal to the product of charge unit rate (t1) by the number of service units (N1) corresponding to this flight.

R1 = t1 x N1

For a given flight, the number of service units (N1) is equal to the product of distance coefficient (d) relative to this flight by the weight coefficient (p) of the considered aircraft.

N1 = d x p

2.1. Distance factor

The distance factor (d) Is equal to the quotient obtained by dividing by one hundred(100) the number of kilometres in the great circle between:

- The aerodrome of departure within, or the entry point into, the airspace defined in the AIP;

- The aerodrome of first destination within, or the exit point of that airspace.

The aforesaid entry and exit points are those at which the lateral limits of the aforesaid airspace are crossed by the flight, these points being chosen taking into account the route the generally used between two aerodromes and, if it is not possible to determine this one, of the shortest route.

2.2 Weight factor

The weight factor (P) is equal to the square root of the quotient obtained aircraft, as set out in the certificate of airworthiness, or the flight manual, or any other equivalent official document as follows:

When the certified maximum take-off weight of the aircraft is not known to the EUROCONTROL, the weight factor shall be calculated on the basis of the heaviest version authorized and supposed to exist for that aircraft.

When an aircraft has multiple certified maximum take-off weights, the weight factor shall be established on the basis of the highest authorized maximum take-off weight for that aircraft by its State of registration.

However, an operator has declared to EUROCONTROL, that he operates two or more aircraft which are different versions of the same type, the weight coefficient for each aircraft of that type used by that operator is determined on the basis of the average of the maximum take-off weights for all his aircraft of that type. The calculation of this weight coefficient per aircraft type and per operator shall be carried out at least once a year.

For the purpose of the charge calculation, the weight coefficient is expressed by a number including two decimals.

2.3 The unit rate

From January 1st 2018, the unit rate established in Euro is: 39,86 Euros.

3. Exempted Flights

The following flights are exonerated from the payment of charge:

a) Flights done by aircraft of which the maximum take-off weight authorized is lower to 5,7 metric tons;

b) Flights done by a state aircraft and that do not imply remuneration of transport;

c) Flights done exclusively for the official missions;

d) Flights operated by the foreign state aircraft, when these States grant the same exemptions to the Moroccan State aircraft;

e) flights of search and rescue;

f) Flights of aircraft and flights exclusively done for the crew training;

g) Flights operated by the officially agreed piloting schools or training centres;

h) Flights having for object to check or to test the air navigation aids;

i) Flights for which the aerodromes of departure and arrival are situated within the same Moroccan territory and they do not imply any intermediate landing or anterior or posterior landing on a foreign territory;

j) Flights of aircraft belonging to the Moroccan aero-clubs;

k) Flights done by a participant in aerial rallye;

l) Flights terminating at the aerodrome from which the aircraft has taken off and during which no intermediate landing has been made.

b) Flights done by a state aircraft and that do not imply remuneration of transport;

c) Flights done exclusively for the official missions;

d) Flights operated by the foreign state aircraft, when these States grant the same exemptions to the Moroccan State aircraft;

e) flights of search and rescue;

f) Flights of aircraft and flights exclusively done for the crew training;

g) Flights operated by the officially agreed piloting schools or training centres;

h) Flights having for object to check or to test the air navigation aids;

i) Flights for which the aerodromes of departure and arrival are situated within the same Moroccan territory and they do not imply any intermediate landing or anterior or posterior landing on a foreign territory;

j) Flights of aircraft belonging to the Moroccan aero-clubs;

k) Flights done by a participant in aerial rallye;

l) Flights terminating at the aerodrome from which the aircraft has taken off and during which no intermediate landing has been made.

4. Methods of payment

4.1

EUROCONTROL invoices and collects the air navigation charges on the users of en-route control services, in accordance to laws and regulations in force in Morocco. These air navigation charges constitute a credit of Eurocontrol.

The person responsible for the payment of the air navigation charge shall be the person who exploited the aircraft at the time when the flight was performed. Where an ICAO call sign is used to identify the flight, the operator of the flight is reputed to be the person to which the ICAO call sign had been allocated at the time of the flight.

If the identity of the operator is unknown, the owner of the aircraft is deemed to be the operator unless he provides which other person was the operator.

If the operator is defaulting, he is jointly responsible with the owner of the aircraft, for charges due.

The charges may be subjected to V.A.T (Value Added Taxes)

Eurocontrol can in this case proceed to the enforced recovery in accordance with the regulations in force in Morocco.

4.2

The charge shall be paid at Eurocontrol’s headquarters in Brussels according to the following conditions of payment.

The amount of the charge is due on the date of performance of the flight. The payment must be received by Eurocontrol at the latest value date shown on the invoice, and is thirty (30) days from the date of the invoice.

Payment shall be put into the bank account of the central service of Eurocontrol en-route charge:

N° 78005192100067311/61 open at the BMCE BANK 140, Avenue Hassan II, Casablanca Morocco. Fast Address: BMCEMAMCA

Except as indicated in the paragraph below, the invoiced amounts shall be paid in Euro (EUR).

The Moroccan users as well as the airlines represented in Morocco can fulfil in Dirhams the charge amounts that are invoiced for them. The payments must be done into the corresponding banking account of the Central Service of Eurocontrol’s en-route charge indicated on the invoice.

When an user avails himself of the facility referred to in the foregoing paragraph, the conversion into Dirhams of Euro (EUR) amounts shall be effected at the daily exchange rate used for commercial transactions for the value date and place of payment.

Payment is deemed to be received by Eurocontrol on the value date on which the amount due was credited into the bank account of the Central Service of Eurocontrol’s enroute charges. The value date is the one on which Eurocontrol may use the funds.

Payments shall be accompanied by an indication giving the references, dates and Euro amounts in respect of invoices paid and credit notes deducted. The requirement to indicate the amounts of invoices in Euro shall apply also to users availing themselves of the facility to pay in Dirhams (MAD).

When a payment is not accompanied by the details specified in paragraph above so to allow its application to a specific invoice(s), Eurocontrol will apply the payment :

- first to interests, and then

- to the oldest unpaid invoices.

5. Claims

5.1

Any claim relating to an invoice must be addressed to Eurocontrol in writing or by an electronic means previously approved by Eurocontrol. The latest date by which the claim must arrive to Eurocontrol shall be indicated on the invoice. The duration in days between this latest date and the date of the invoice is the same as in the system of en-route charges of Eurocontrol.

The date of submission of claims shall be the date of their receipt by Eurocontrol.

Claims must be detailed and should be accompanied by any appropriate supporting evidence.

Submission of a claim by an user shall not entitle him to make any deduction from the invoice in question unless so authorised by Eurocontrol.

Where Eurocontrol and an user are mutually debtor and creditor, no compensatory payment shall be effected without Eurocontrol’s prior agreement.

5.2 Penalties for late payments

Any en-route charge that has not been paid by its due date shall be increased by penalty at simple rate of 8.43 % per year. The interest, entitled interest on late payment, shall be simple interest calculated from day to day on the unpaid overdue amount. This interest shall be calculated and invoiced in Euros.

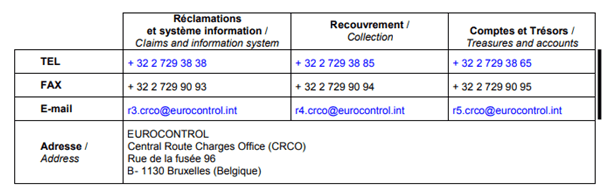

6.Contact